Live from the Wiener Stadthalle press centre — as the SF2 jury show begins tonight at 21:00 CEST and 15 more countries learn their Grand Final fate on Thursday, the most striking data point on our screens this morning is not from the bookmakers. It is from Polymarket.

18+ | New customers only | T&Cs apply | Please gamble responsibly

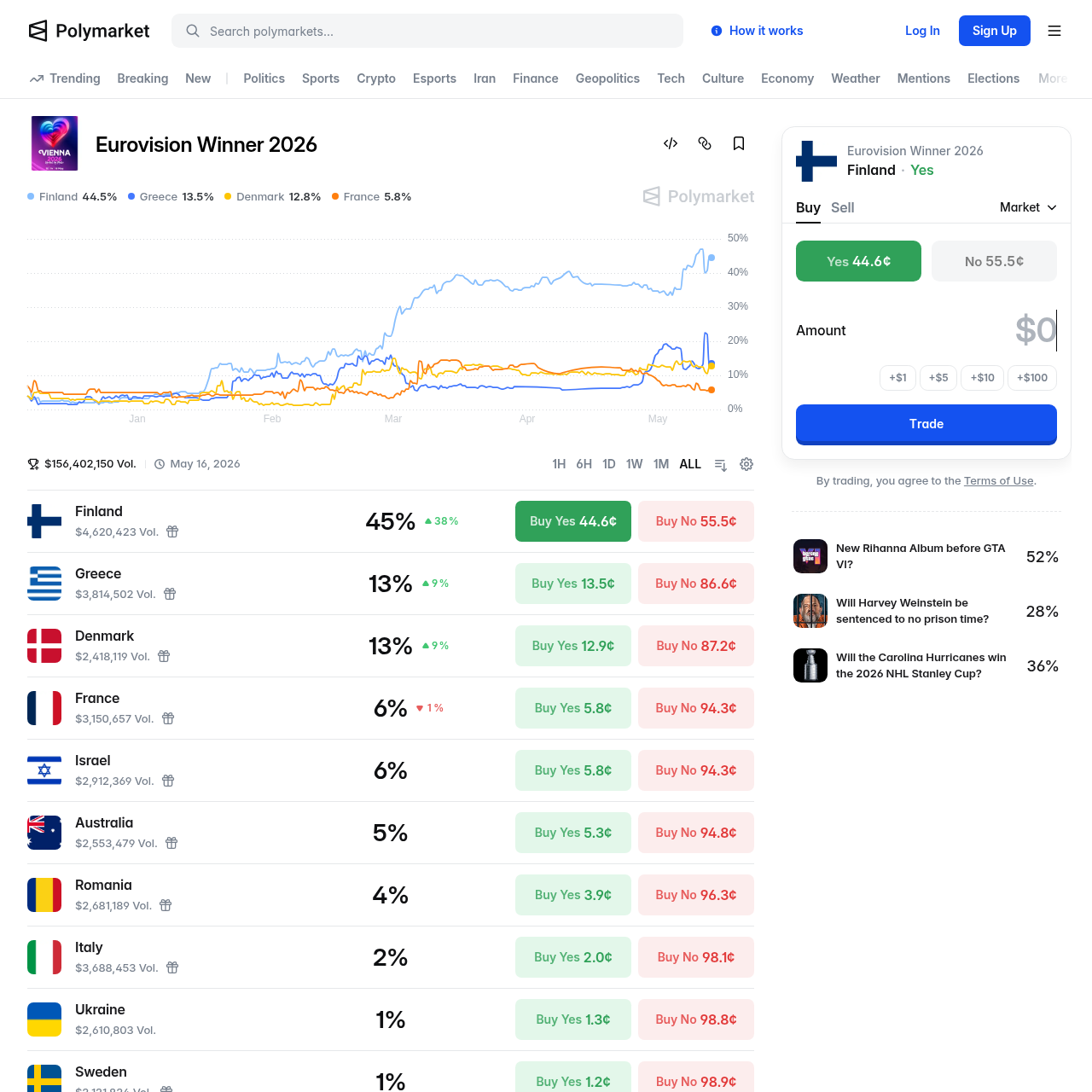

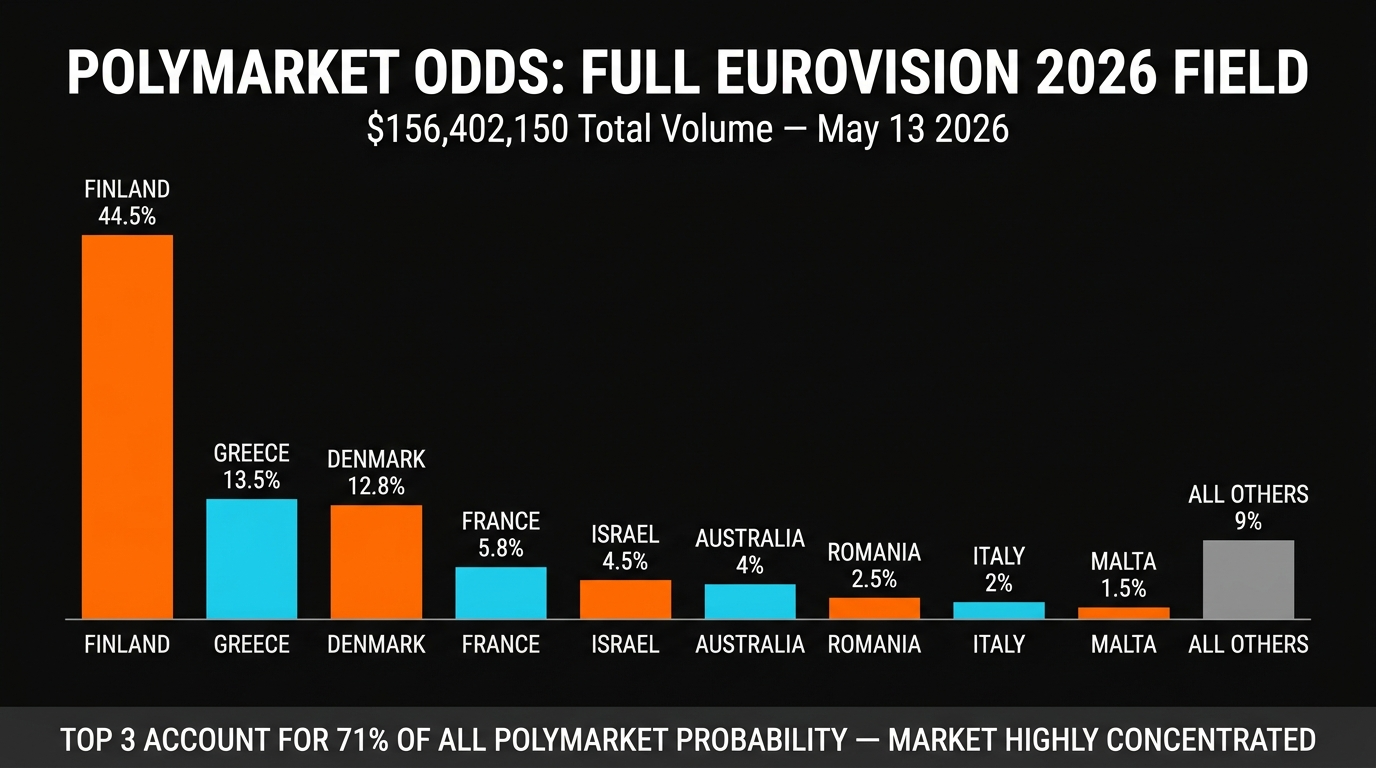

As of 13:30 CEST on Wednesday May 13, the prediction market has now traded $156,402,150 on Eurovision 2026 winner contracts — up from $113 million one week ago. That is a 38% increase in trading volume in seven days, driven by the escalation of news from the Wiener Stadthalle: first rehearsals, second rehearsals, SF1 qualification, and the Grand Final running order draw.

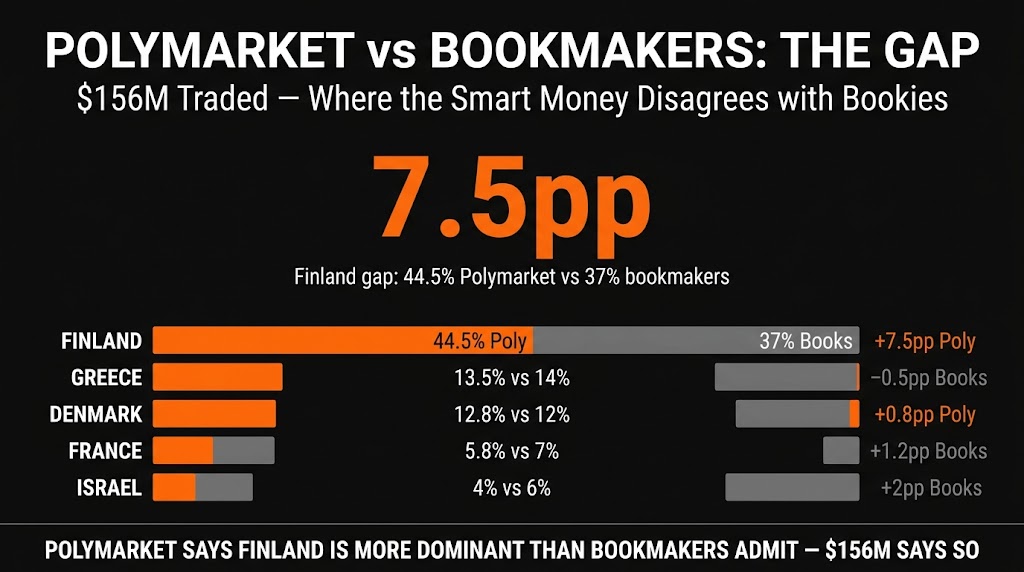

The data tells a clear story: Polymarket and bookmakers agree on the overall shape of the market — Finland leads, Greece second, Denmark third — but they disagree materially on the magnitude of Finland's advantage. Finland sits at 44.5% on Polymarket versus 37% on bookmakers. That 7.5 percentage-point gap is the largest divergence of any finalist in this contest, and understanding why it exists is the key to finding value before Saturday.

Betfred — Bet £10 Get £50 in Free Bets on Eurovision 2026

The Full Divergence Table: Who Polymarket Believes In More

Prediction markets and bookmakers approach probability estimation differently. Bookmakers set prices to balance their book — they adjust odds to equalise liability, not necessarily to reflect their own probability assessment. Polymarket is a pure market: traders buy and sell binary outcome contracts at prices set by supply and demand, with no bookmaker margin embedded in the price.

When the two systems diverge significantly, it typically means one of three things: bookmakers are protecting their liability on a heavily-bet favourite; Polymarket traders have materially different information or interpretation; or a recent event has shifted the market and the two systems are adjusting at different speeds.

| Country | Polymarket | Bookmaker avg | Divergence | Interpretation |

|---|---|---|---|---|

| Finland | 44.5% | 37% | +7.5pp Poly | Polymarket pricing in Producer's Choice late-slot premium |

| Greece | 13.5% | 14% | −0.5pp | Near-consensus on #2 despite First Half draw |

| Denmark | 12.8% | 12% | +0.8pp Poly | Marginal Poly premium; SF2 draw unknown still |

| France | 5.8% | 7% | +1.2pp Books | Bookmakers slightly more bullish on Monroe jury appeal |

| Israel | ~4.5% | 6% | +1.5pp Books | Polymarket traders discount Israel re: boycott exposure |

| Australia | ~4% | 5% | +1pp Books | Books slightly higher on Delta Goodrem jury appeal |

| Romania | ~2.5% | 3% | +0.5pp Books | Near-consensus on 7th place ceiling |

| Italy | ~2% | 3% | +1pp Books | Books somewhat more bullish on Sal Da Vinci Sanremo bump |

Data: Polymarket and Eurovisionworld.com, verified 13:30 CEST May 13 2026.

Why the 7.5pp Finland Gap Exists

The Finland divergence is not random noise. Four structural factors explain why Polymarket is pricing Finland materially higher than bookmakers at this precise moment:

1. The Producer's Choice draw (announced May 12). Finland drew Producer's Choice in last night's Grand Final running order draw. This means ORF — the Austrian host broadcaster — will place Finland wherever they choose in the 26-slot running order. Every credible analysis points to a late second-half position, likely slots 22-25. Late-slot placement historically adds approximately 15-20 percentage points to an act's televote performance relative to an equivalent mid-first-half placement. Polymarket traders appear to have priced this in immediately; bookmaker liability management means they adjust more slowly.

2. Polymarket has no liability to manage. Bookmakers adjust odds to balance their exposure across all possible outcomes. When Finland is the most-backed outright winner by betting volume — as they are at every major bookmaker — the bookie is incentivised to make other outcomes look attractively priced to draw counter-bets. This artificially suppresses Finland's displayed probability relative to pure market belief. Polymarket has no such incentive: the 44.5% reflects what informed traders are willing to pay for a binary Finland-wins contract.

3. The SF1 result reinforced Finland's dominance. Finland qualified from SF1 with what observers in the press room described as one of the strongest live vocal performances of the contest. The staging — featuring the live violin element that was the subject of an EBU exception ruling — delivered exactly as rehearsed. No other SF1 qualifier materially improved relative to Finland's ceiling. The bookmaker market reflects pre-SF1 positioning more than Polymarket, which adjusts in real time.

4. $156M of informed money. Polymarket's volume on Eurovision has grown 38% in seven days. The marginal traders entering the market at this stage — as opposed to speculators who placed positions months ago — are disproportionately informed bettors who follow the contest closely. Their consensus is 44.5% for Finland.

Stake — Back Finland at 2.10 Before the Market Closes the Gap

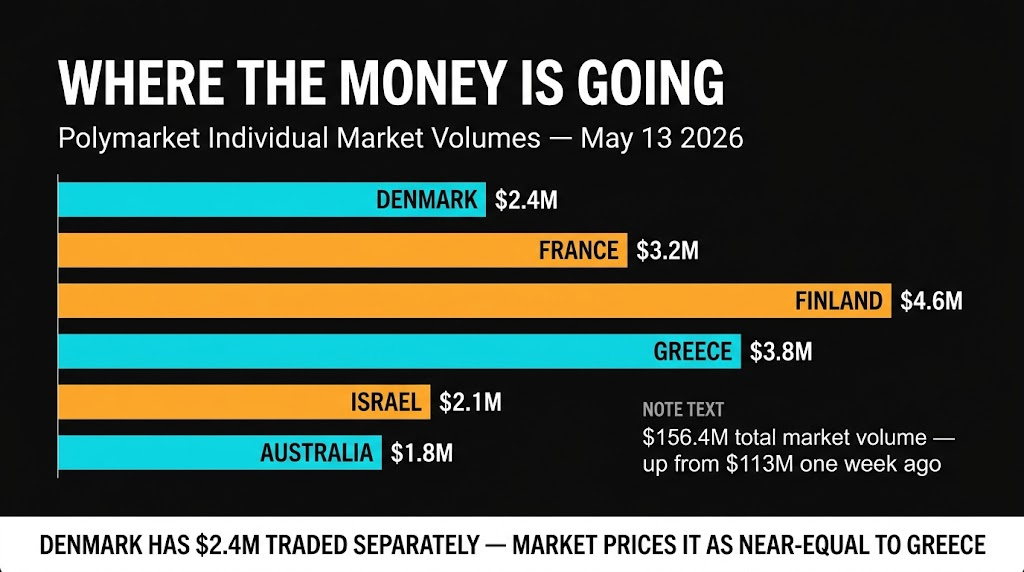

The Volume Story: Where $156M Went

Individual Polymarket country markets provide an additional layer of signal: how much money is actually trading on each country tells you how seriously the market takes each candidate. High volume = tight spreads = more reliable price. Low volume = thin market = easier to distort.

| Country | Polymarket Individual Vol. | Win Probability | Confidence Level |

|---|---|---|---|

| Finland | $4.62M | 44.5% | High — largest individual market |

| Greece | $3.81M | 13.5% | High — second deepest market |

| France | $3.15M | 5.8% | High — disproportionate to probability |

| Denmark | $2.42M | 12.8% | High — nearly equal to Greece volume |

| Israel | $2.10M | ~4.5% | Medium-high — politically motivated volume |

| Australia | $1.80M | ~4% | Medium — jury market premium interest |

Data: Polymarket individual country markets, May 13 2026. Individual volumes sum to less than total because total includes the grouped market.

Two observations stand out from the volume data. First, France has attracted $3.15M in volume despite sitting at just 5.8% win probability. This outsized volume relative to probability suggests France is generating significant speculative interest — either as a hedge against Finland underperforming, or because traders believe the bookmaker's 7% price is closer to correct than Polymarket's 5.8%. This is one of the cleaner arbitrage reads: if you believe France is more likely than 5.8%, the bookmaker price of 7% is the better expression.

Second, Denmark and Greece have nearly equal volumes ($2.42M vs $3.81M) despite a 0.7pp gap in their probabilities. The market is treating them as close to interchangeable in terms of their realistic ceiling — both are strong second-tier contenders but neither challenges Finland's structural dominance. The betting question is which of the two offers better each-way value, not which is the true #2 vs #3.

The Greece Case: First Half Draw Meets Jury Floor

Greece drew First Half in last night's Grand Final running order draw. Polymarket currently prices Greece at 13.5%, fractionally below the bookmaker average of 14%. The lack of a significant Polymarket discount relative to books suggests traders are not yet fully pricing in the first-half penalty — or they believe Greece's jury floor makes the structural disadvantage tolerable.

Historical data on this is instructive. Since 2016, the three first-half entries that have finished on the podium all had either: (a) dominant diaspora voting blocs that don't rely on recency bias, or (b) jury-heavy scoring profiles that compensated for the televote shortfall. Greece qualifies on criterion (b). Ferto is expected to land top-3 with professional juries; the question is whether that jury ceiling translates to enough overall points from a first-half position to reach the podium.

For betting purposes, the Greece first-half draw creates a specific opportunity: the each-way market (top-3 finish) is more efficiently priced than the outright. Greece's jury floor means they are unlikely to finish below 5th regardless of running order position. Their second-place finish probability, however, is reduced by first-half placement. The optimal exposure is top-3 each-way, not outright winner.

Denmark: The Unknown Variable

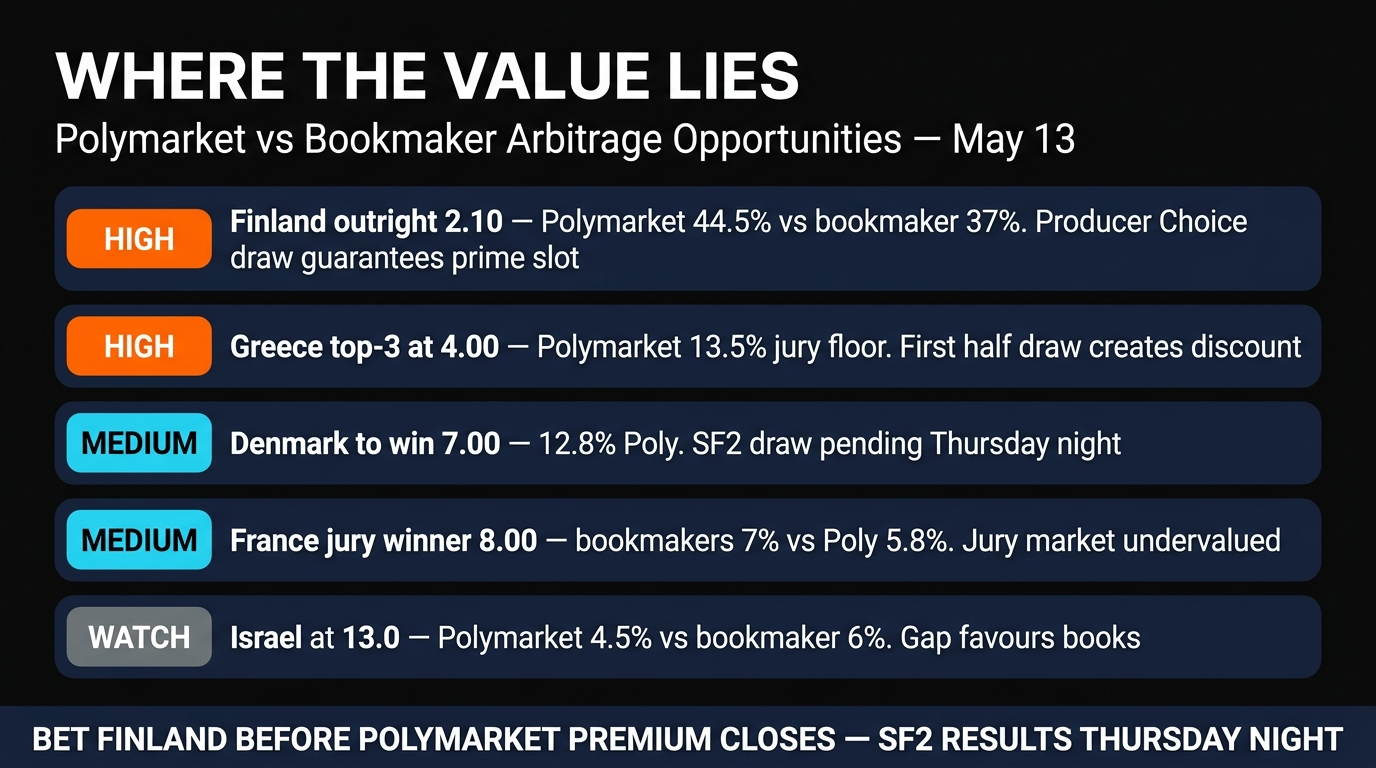

Denmark (Søren Torpegaard Lund, Før vi går hjem) sits at 12.8% on Polymarket and 12% on bookmakers — the #3 favourite in both markets. Their Grand Final running order draw has not yet happened: they are in SF2, which means they draw Thursday after the broadcast.

The Thursday draw result is material. If Denmark draws Producer's Choice or Second Half, their 12% probability is well-founded and possibly conservative — Før vi går hjem is a strong jury and televote act with broad European appeal. If Denmark draws First Half, their probability should discount in a similar manner to Greece: perhaps 2-3pp lower than current. The current market price implies traders are assuming Denmark will draw a favourable position — which at 66% likelihood (two-thirds of outcomes are Second Half or Producer's Choice) is a reasonable baseline assumption but not a certainty.

How to Use the Polymarket-Bookmaker Gap

The gap analysis leads to concrete betting positions. Where Polymarket is higher than bookmakers, the prediction market is pricing in information or structural factors the bookmaker hasn't yet adjusted for. Where bookmakers are higher, they may be holding liability-driven prices or holding pre-event assessments.

The actionable framework:

- Finland at 2.10 (bookmakers): Polymarket at 44.5% implies a fair price of approximately 2.25. The bookmaker is offering 2.10 — shorter than Polymarket's implied fair value but reflecting real structural advantages (Producer's Choice draw, SF1 qualifying performance) that justify the premium. This is a back, not a lay.

- Greece top-3 each-way at ~4.00: Polymarket and books are aligned at 13.5-14% outright, but the each-way market at 4.00 offers implied 3× the top-3 probability — more efficient than the outright given the first-half draw penalty.

- France at 7% (books) vs 5.8% (Poly): The bookmaker price of 7% reflects Monroe's genuine jury appeal better than Polymarket's 5.8%. This is a market where books offer better value — if you believe France has a jury ceiling, the bookmaker price is the right vehicle.

- Israel at 10.00-17.00: Books (6%) price Israel materially higher than Polymarket (~4.5%). The 1.5pp gap is attributable to Polymarket traders discounting Israel's real win probability for non-betting reasons (political sentiment). The bookmaker price is arguably more accurate.

Thunderpick — Bet on Eurovision 2026 With Crypto

Betting Recommendations: The Polymarket Lens

| Bet | Bookmaker Price | Polymarket Implied Fair | Verdict |

|---|---|---|---|

| Finland outright winner | 2.10 (37%) | 2.25 (44.5%) | HIGH — Polymarket says bookie is short of true probability but structural case is strong regardless |

| Greece top-3 each-way | ~4.00 top-3 | ~3.50 (top-3 implied) | HIGH — first half draw discount not yet in each-way price |

| Denmark outright | 6.50-7.00 (12%) | 7.80 (12.8% Poly) | MEDIUM — monitor Thursday draw; second half or Producer's Choice draw tightens |

| France outright | 11.00-13.00 (7%) | 17.00 (5.8% Poly) | MEDIUM — bookmaker price superior to Polymarket; jury ceiling is real |

| Israel outright | 10.00-17.00 (6%) | 22.00 (4.5% Poly) | MONITOR — Producer's Choice slot uncertainty adds variance |

| Australia jury winner | 3.50-4.00 | — | MEDIUM — no Polymarket jury market; Delta Goodrem jury floor still strong |

All odds from bookmaker aggregates at Eurovisionworld.com and Polymarket, verified May 13 2026.

Cloudbet — Bitcoin Betting on Eurovision 2026 Grand Final

Frequently Asked Questions

What is Polymarket and how does it work for Eurovision betting?

Polymarket is a decentralised prediction market where users trade binary outcome contracts. For Eurovision, each contract pays $1.00 if that country wins and $0.00 if they don't. The market price (e.g., 44.5¢ for Finland) represents the market's collective probability estimate. Unlike bookmakers, Polymarket has no margin built in — prices are set purely by supply and demand from traders worldwide. $156.4 million has now been traded on Eurovision 2026 winner contracts.

Why is Finland's Polymarket probability so much higher than bookmakers?

Three main reasons: (1) Polymarket adjusts in real time, and has already priced in Finland's Producer's Choice draw from last night — bookmakers adjust more slowly due to liability management. (2) Bookmakers artificially suppress Finland's displayed probability to attract counter-bets and balance their exposure. (3) Polymarket's marginal traders at this stage of the contest are disproportionately informed bettors who have followed the rehearsals and see Finland's structural advantages clearly.

Does the Polymarket-bookmaker gap mean Finland is definitely going to win?

No. A 44.5% probability, even if entirely accurate, means Finland loses 55.5% of the time. The gap analysis is a tool for identifying where value lies — not a guarantee of outcome. The gap suggests the bookmaker price of 2.10 (37%) is conservative relative to the prediction market consensus, which implies a fair price of approximately 2.25. The case for backing Finland rests on the Producer's Choice draw, SF1 performance quality, and Liekinheitin's broad jury and televote appeal — not simply on Polymarket being higher than books.

When should I expect the biggest odds movements before Saturday?

Two key windows: (1) Thursday night, after SF2 concludes and the remaining 12 countries draw their Grand Final slots. Denmark, Australia, Romania, France, and the UK will all draw — with Denmark's and France's results having the most significant market impact. (2) Friday evening, once the full Grand Final running order is published by ORF. The running order reveal will cause markets to adjust for slot positions — specifically for Finland, who will be confirmed in whatever late slot ORF has chosen.

Is it worth waiting for Thursday's draw results before betting?

For Finland: no. Their Producer's Choice draw is confirmed; their late-slot placement is effectively guaranteed. The price is unlikely to improve after Thursday — it is more likely to shorten further as the full picture becomes clearer. For Denmark and France: yes, waiting until after their draw results is the rational strategy. A Denmark First Half draw would create a similar discounted opportunity to what Greece currently presents.

Related Articles

- Polymarket Eurovision 2026: $113 Million Traded — Prediction Market Analysis

- Grand Final Running Order Draw: Finland Producer's Choice and Greece First Half Betting Analysis

- Eurovision 2026 Running Order Impact Analysis: Why Position Matters More Than Ever

- Why Finland Will Win Eurovision 2026: Liekinheitin Full Betting Analysis

- Eurovision 2026 Jury vs Televote Betting Strategy

- Eurovision 2026 Each-Way Betting Tips and Value Picks

All odds sourced from Eurovisionworld.com and Polymarket, verified May 13 2026. 18+. Please gamble responsibly. BeGambleAware.org