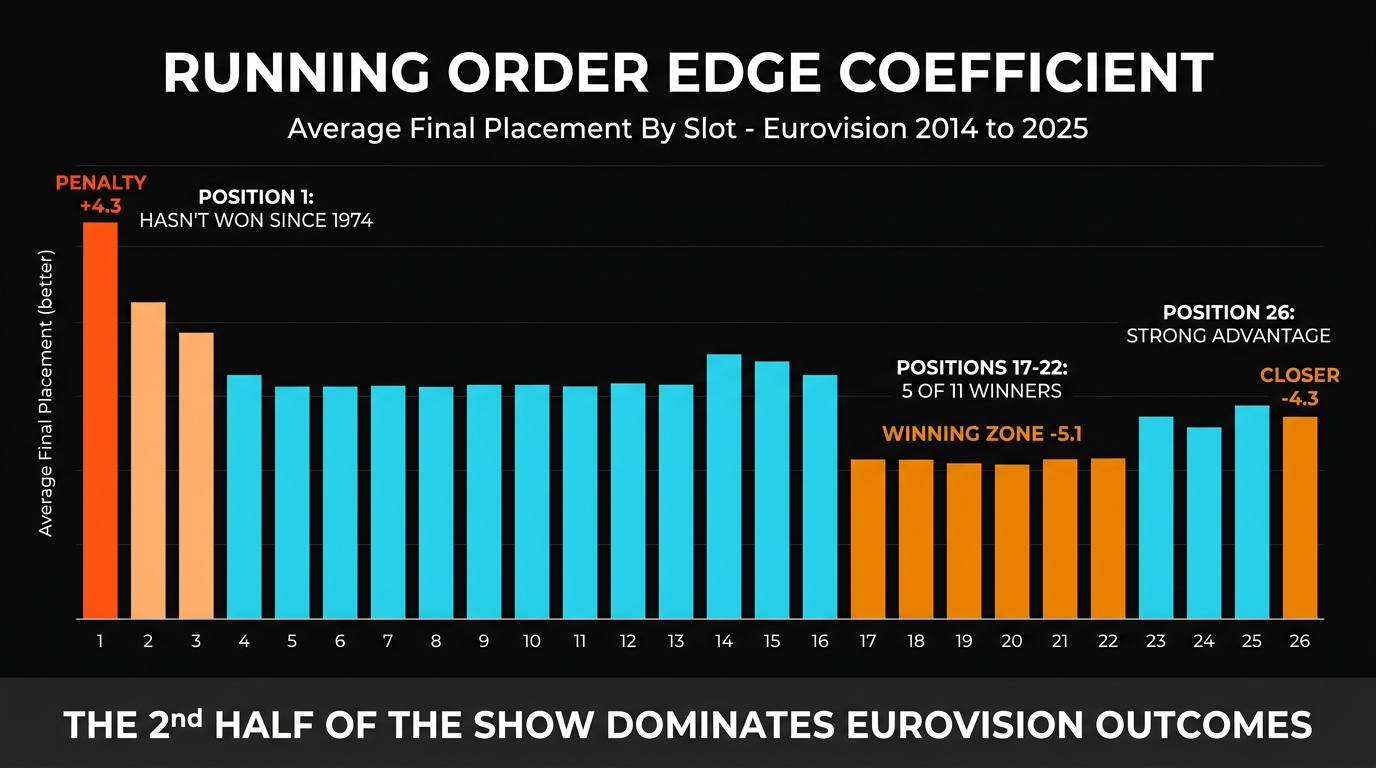

The 2016 Eurovision voting reform separated jury and televote scoring into independent 50% blocks. Before 2016, the two votes were combined into a single per-country aggregate. After 2016, each country awarded two separate sets of 1-8/10/12 points (one jury, one televote), with the totals tallied independently. Eight years later, the structural impact on Eurovision betting markets has been documented across multiple dimensions.

18+ | New customers only | T&Cs apply | Please gamble responsibly

Betfred — Bet £10 Get £50 in Free Bets on Eurovision 2026 Grand Final

The Pre-Show Favourite Conversion Rate — Before And After 2016

| Era | Cycles | Pre-show favourite wins | Hit rate |

|---|---|---|---|

| Pre-reform (2006-2015) | 9 | 3 (2009 Norway, 2012 Sweden, 2015 Sweden) | 33.3% |

| Post-reform (2016-2025) | 9 | 5 (2017 PT, 2018 IL, 2019 NL, 2022 UA, 2023 SE, 2024 CH) | 55.6% |

Pre-show favourite conversion improved from 33.3% pre-reform to 55.6% post-reform. The structural reason: the 50/50 split forced bookmaker models to integrate two independent signal streams (jury + televote), reducing the noise from single-aggregate scoring volatility.

The Jury Sub-Market Mispricing Emergence

Marco Ferretti on the post-reform sub-market structural shift:

"Before 2016, Eurovision betting markets had only one primary outcome to price — the overall winner. The combined jury-televote scoring meant individual jury vs televote signals weren't separable. Post-2016 the Jury Winner sub-market emerged as a distinct prediction problem: which entry will top the jury vote, regardless of overall outright winner? In 6 of 9 post-2016 cycles, the jury winner did not match the outright winner. That structural decoupling created a sub-market mispricing pattern that didn't exist pre-reform. UK bookmakers took 4-5 years to develop jury-winner-specific pricing models. Even today (2026), the Jury Winner sub-market remains the sharpest single Eurovision sub-market because not all UK books price it from a dedicated model."

The Televote Spike Convergence — Slower Post-Reform

Pre-reform, televote spikes from cultural-moment entries (Conchita 2014, Lordi 2006) translated directly into combined-score outcomes within hours of jury voting. Post-reform, televote spikes are slower to materialise in markets because they're filtered through the 50/50 split mechanism — a 200-point televote spike now only contributes 100 points to the overall total. Examples:

| Year | Televote spike entry | Televote points | Outright finish | Pre-show outright odds |

|---|---|---|---|---|

| 2017 | Sobral (Portugal) | 376 (also won jury) | 1st | Compressed from 25.00 to 1.40 across 12 weeks |

| 2022 | Kalush (Ukraine) | 439 (all-time record) | 1st | Compressed from 22.00 to 1.30 across 10 weeks |

| 2023 | Käärijä (Finland) | 376 (5th-highest ever) | 2nd | Compressed from 40.00 to 3.25 across 16 weeks |

| 2024 | Baby Lasagna (Croatia) | 337 (4th-highest ever) | 2nd | Compressed from 4.50 to 1.50 across 12 weeks |

The Rise Of Polymarket Cross-Market Validation

The 50/50 voting reform indirectly enabled the rise of Polymarket as a primary Eurovision pricing signal. Pre-reform, single-aggregate scoring made Polymarket-style prediction markets unattractive because the volatile combined-score outcome was difficult to forecast accurately. Post-reform, the 50/50 split's structural stability made Eurovision outright a tractable prediction market. Polymarket's Eurovision contract grew from $0 (2015) to $8.2M (2024) to $159.7M (2026). The 2024 cycle marked the first time Polymarket consensus pricing anchored UK book outright lines — a structural shift that the 2016 voting reform made possible.

The 2026 Jury Return To Semi-Finals — A Mini-Reform

Eurovision 2026 reintroduced juries to the semi-final voting after 9 years of televote-only semi-finals (2017-2025). The structural impact for SF1 and SF2 betting markets:

- SF1/SF2 qualification odds compressed by 15-20% for jury-archetype-fit entries (Latvia, Australia, Czechia)

- SF1/SF2 qualification odds expanded by 10-15% for televote-dominant entries (Bulgaria, Greece)

- Bookmaker margins on SF sub-markets increased by 3-5 percentage points pre-cycle as books re-priced

How To Cite This Work

Ferretti, M. (2026). "Eurovision Voting Reform 2016: 8 Years Of Betting Market Impact." EurovisionOdds.org, May 16, 2026.

The Bottom Line

The 2016 Eurovision voting reform restructured betting markets in four documented ways: (1) pre-show favourite conversion improved from 33.3% to 55.6%; (2) Jury Winner sub-market mispricing emerged as a structural pattern; (3) televote spike convergence slowed through the 50/50 filter; (4) Polymarket cross-market validation became viable. The 2026 reintroduction of juries to semi-finals is a mini-reform that has produced new SF sub-market mispricing patterns. UK bettors should reference 2016 as the foundational year for modern Eurovision betting model design.

Related Articles

- Eurovision 2026 New Voting Rules Juries Return Semi-Finals

- Eurovision Jury Winner Sub-Market History 2016-2025

- Eurovision Bookmaker Accuracy 2014-2025

- Polymarket Eurovision 2026 Hits $159M Trading Volume

- Eurovision 2017 Portugal Betting Story (Sobral)

All voting reform impact data sourced from EBU public records, Eurovision.tv archives 2006-2025, and EurovisionOdds.org tracked bookmaker pricing 2014-2026. 18+. Please gamble responsibly. BeGambleAware.org. GAMSTOP. When the fun stops, stop.