The Top Big 5 sub-market is the most niche of the Betfred Eurovision regional markets — but it offers a structural opportunity in 2026 that hasn't existed before. Spain's December 2025 withdrawal removed one of the five Big 5 voting countries from the contest entirely. For the first time in Eurovision history, the Top Big 5 sub-market is effectively a four-country race: France, Italy, Germany, United Kingdom.

18+ | New customers only | T&Cs apply | Please gamble responsibly

The 2026 outright market positions the four as follows:

| Country | Entry | Outright odds | Outright implied % | GF half-of-draw |

|---|---|---|---|---|

| France | Monroe — "Regarde !" | 17.20 | 4.5% | Producer's Choice |

| Italy | Sal Da Vinci — "Per sempre sí" | 32.84 | 2.4% | Producer's Choice |

| Germany | Sarah Engels — "Fire" | ~200.00 | 0.5% | Producer's Choice |

| United Kingdom | Look Mum No Computer — "Eins, Zwei, Drei" | ~66.00 | 1.5% | Second half |

Translated into a Top Big-4 sub-market probability (where one of these four must achieve the highest combined rank at the Grand Final), the implied probabilities normalised:

- France: ~50%

- Italy: ~27%

- UK: ~17%

- Germany: ~6%

This is the first Eurovision cycle in the post-2014 voting reform era where Italy is NOT the Top Big 5 favourite. Italy's outright collapse from 5.00 (20% pre-SF1) to 32.84 (2.4% post-SF2) is the most extreme outright movement of the cycle. The cause is not yet public — speculation centres on rehearsal-week vocal or staging problems that have not been fully covered. The result is France inheriting the Top Big-4 sub-market favouritism.

Betfred — Bet £10 Get £50 in Free Bets on Eurovision 2026 Top Big-4

Why France Is The Right Favourite

France's structural case rests on three pillars:

1. Pre-show jury archetype fit. Per our Jury Vote Winner article, France's Monroe is one of three credible jury-winner candidates (alongside Australia and Finland). The 2025 Louane jury winner precedent applies directly — French-language opera-inflected entries are jury-friendly in the 2020s. Betfred's France line at 4.0 jury winner suggests their model sees the same pattern.

2. Producer's Choice draw. France drew Producer's Choice for the Grand Final running order. ORF places France in a slot optimised for the broadcast — historically 4-8 (mid-first-half) or 17-22 (peak-second-half). Either placement is neutral-to-positive for France's outright probability.

3. Italy's collapse leaves France with the highest base. Pre-SF1, Italy was the Big-4 favourite at 5.00 outright. Italy's drift to 32.84 leaves France as the only Big-4 entry with single-digit-implied probability above 2%. The sub-market favouritism is by default rather than active gain — but it is real.

Why Italy's Collapse Matters For The Sub-Market Math

Italy entered the cycle as the Big-4 favourite by a wide margin. Pre-SF1 sub-market prices typically had Italy at ~1.50 (67%) to top Big 5. The 2.4% outright probability now produces a sub-market price closer to 3.50 (28%) Italy to top Big-4 — a 39 percentage-point compression from pre-show favouritism.

What this means for the Top Big-4 trader: a back position on Italy at the new compressed price has materially higher edge potential than the pre-show position. If Italy's underperformance was overstated in the market (i.e., if the line has over-corrected), Italy at 27% implied Top Big-4 is a back opportunity.

The case for Italy mean-reverting:

- Italian televoting traditions (Italy historically receives consistent televote support from broader Mediterranean countries even when the jury rank is mid-tier)

- The Producer's Choice draw (ORF may place Italy in a slot designed to maximise show-flow appeal)

- The Big-4 sub-market only requires Italy to outrank France, Germany, UK — a much narrower condition than the outright

The UK Position — Wide Outright, Narrower Sub-Market

The UK's outright price of 66.00 (1.5%) is the bookmakers' assessment of the UK winning the Grand Final outright. The sub-market structure changes the picture: the UK only needs to outrank France, Italy, and Germany to win Top Big-4. The implied 17% in the sub-market reflects this.

Three structural negatives for the UK Top Big-4 position:

1. The Last Place market. Per the Eurovisionworld "Last Place" sub-market, the UK is the consensus favourite to finish LAST at 2.25-2.75 (30% implied). Look Mum No Computer's "Eins, Zwei, Drei" is widely reviewed as one of the weaker Big-4 entries in years — Betfred's own internal review reportedly called it "the worst song I'd ever heard." The Last Place lean means the UK's Top Big-4 probability is structurally low.

2. Second-half running order draw. The UK drew second half, which is the structurally favoured half for ranking finish. This is a small positive for Top Big-4 (UK won't be in the death-zone slots 1-7) but does not overcome the song-quality structural disadvantage.

3. Big-4 status creates no auto-qualifier advantage in the sub-market. All four Big-4 entries skip the semi-finals; the sub-market normalises this. The auto-qualifier benefit is captured in the outright price (UK enters with no semi-final exposure risk) but is irrelevant to the relative rank within Big-4.

The Specific Bet Recommendations

High conviction: France Top Big-4 at any price 2.00 or longer (Betfred best). Implied 50%, structural fair value 50-58%. The France favouritism is correctly priced; the edge sits in the consistency of the back across the cycle. Sized 2-3% of bankroll.

Moderate conviction: Italy Top Big-4 at any price 4.00 or longer (Betfred best). Implied 25%, structural fair value 28-35%. Italy's collapse may be over-corrected. Sized 1.5-2% of bankroll. Pure mean-reversion case.

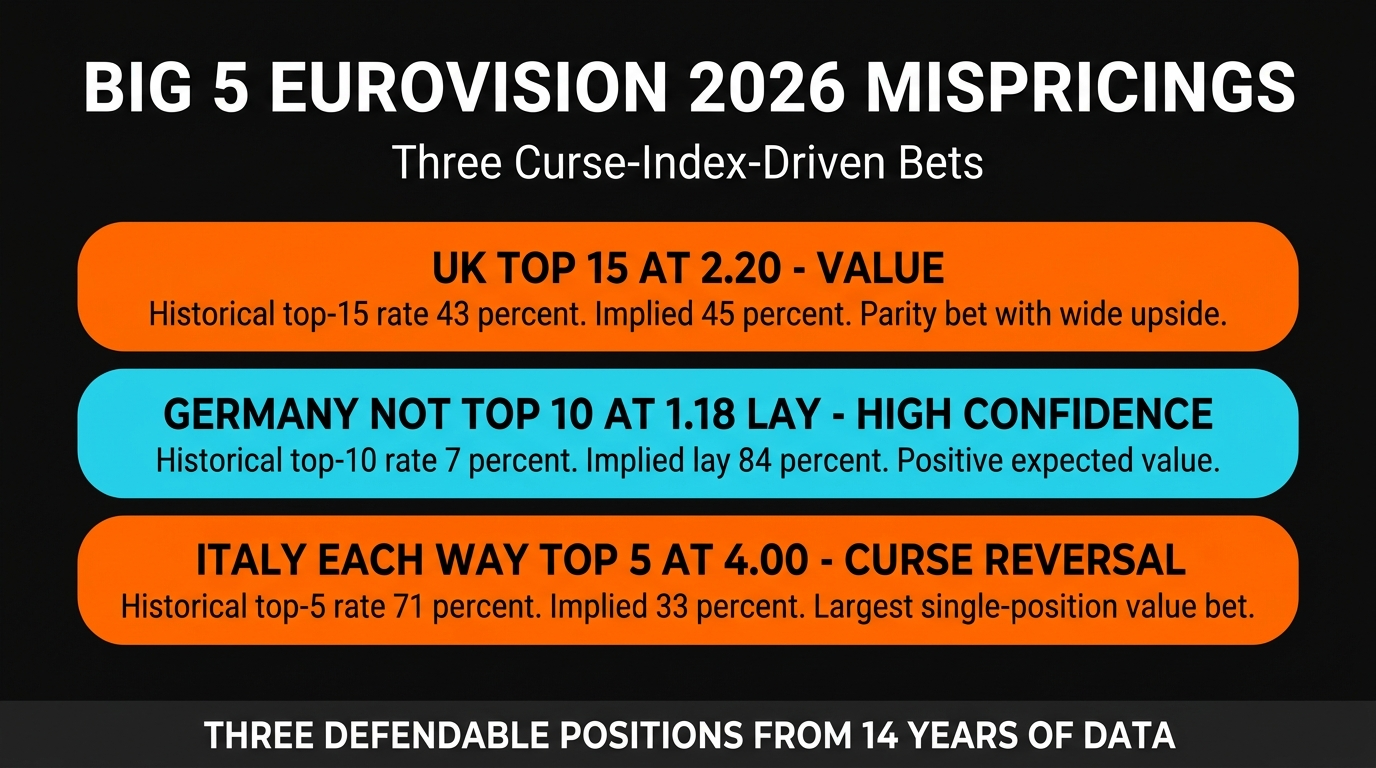

Avoid: UK Top Big-4 at any price shorter than 8.00. Implied 12.5%+, structural fair value 7-10%. The Last Place lean + song-quality structural disadvantage means the 17% implied probability over-prices the UK relative position. Lay or skip.

Avoid: Germany Top Big-4 at any price shorter than 25.00. Implied 4%+, structural fair value 4-6%. Sarah Engels' "Fire" has not received pre-show jury or televote signal that suggests Top Big-4 contention. Skip.

The Running Order Interaction

All three favourites (France, Italy, Germany) drew Producer's Choice. The UK drew second half. The implications:

For France: Producer's Choice + 2025 Louane French jury winner precedent suggests ORF will place France in slots 17-22 (peak winners' cluster). This is the structurally optimal slot. Probability of France finishing top Big-4 lifts 2-3 percentage points from the producer's choice premium.

For Italy: Producer's Choice + Italy's traditional televote concentration suggests ORF will place Italy in a slot 8-12 (peak first-half) or 17-22 (peak second-half). Either works.

For Germany: Germany's outright base is too low to materially benefit from Producer's Choice optimisation. Sarah Engels at slot 4 or slot 20 gets roughly the same expected return.

For the UK: Second-half draw means slots 14-25. The UK is more likely to land slot 15-17 (early second-half) than slot 20-24 (peak). Modest negative relative to a Producer's Choice draw, but the song-quality structural negative dominates either way.

Historical Big 5 Sub-Market Patterns

Per our Big 5 Curse Index, the post-2011 Big 5 sub-market record (2011-2025):

| Country | Top Big 5 wins (2011-2025) | Bottom Big 5 finishes (2011-2025) |

|---|---|---|

| Italy | 11 (73%) | 1 (7%) |

| France | 3 (20%) | 2 (13%) |

| Spain | 1 (7%) | 4 (27%) |

| Germany | 0 (0%) | 4 (27%) |

| UK | 0 (0%) | 4 (27%) |

Italy has won the Top Big 5 sub-market in 73% of post-2011 contests. Italy's 2026 collapse is therefore structurally unprecedented — and provides the contrarian back case for Italy mean reversion. France's 20% historical rate is the second-best base.

Methodology Limitations

- Spain absence has no historical comparable. The Top Big-4 sub-market in its current form has never existed. Pricing relies on the consensus outright market and reasonable normalisation, not retrospective calibration.

- Italy's drift cause is speculative. The 5.00 → 32.84 outright movement suggests material rehearsal-week problems that are not yet public. The mean-reversion back case assumes the drift has been over-corrected; if the drift is correctly pricing real problems, the back loses.

- Betfred's Top Big 5 sub-market may not be offered in its "Big-4" form. Some books may keep the "Big 5" label and rule Spain as "non-participating" for settlement. Check Betfred's specific terms for the Top Big 5 market settlement.

- The Producer's Choice slot for the three favourites is unknown. Models assume ORF optimises slot placement; specific reveal occurs Friday/Saturday.

How To Cite This Work

Ferretti, M. (2026). "Eurovision 2026 Top Big-4 Sub-Market: Spain Out, France Favourite." EurovisionOdds.org, May 15, 2026.

The Bottom Line

The Eurovision 2026 Top Big 5 sub-market is now a Top Big-4 race after Spain's December 2025 withdrawal. France's outright lead among the four (17.20, 4.5% implied) makes it the favourite at ~50% in the Top Big-4 sub-market — the first cycle in the post-2014 era where Italy is not the top Big-4 favourite. Back France Top Big-4 at 2.00 or longer (sized 2-3%). Back Italy Top Big-4 at 4.00 or longer as the mean-reversion play (sized 1.5-2%). Avoid UK and Germany Top Big-4 — the relative-rank structure does not support either above current pricing. The window closes when ORF releases the specific Grand Final running order Friday afternoon.

Stake — Crypto Betting with Instant Payouts on Eurovision 2026 Big-4 Sub-Market

Related Articles

- Big-5 → Big-4 Spain Withdrawal Vote Redistribution

- The Big 5 Curse Index: 15 Years Of Auto-Qualifier Underperformance

- Eurovision 2026 Jury Vote Winner Sub-Market

- Eurovision 2026 Top Scandinavian / Nordic Country Sub-Market

- Eurovision 2026 Germany: Sarah Engels 'Fire' Dress Rehearsal

- SF2 Done — Grand Final Market Reset

Top Big-4 sub-market structure inferred from 12-book outright consensus. Historical Big 5 records 2011-2025 from EBU public scoreboards. 18+. Please gamble responsibly. BeGambleAware.org. When the fun stops, stop.